A landmark general election in India, scheduled for the summer of 2024, will see the drivers of economic growth shift midway through the year, according to Goldman Sachs Research. Overall, despite food and oil supply shocks keeping inflation elevated, growth is forecast to remain stable and resilient.

For 2023, our economists expect real GDP growth to come in at 6.7% year on year, up from our earlier estimate of 6.4%. Among the 13 large economies in Goldman Sachs Research’s global outlook for 2024India’s projected growth rate is the highest at 6.2%, with China in second at 4.8%, as of December 18. As the 2024 election approaches, “we expect consumption growth to be driven by subsidies and transfer payments,” write Goldman Sachs Research’s India economists Santanu Sengupta and Arjun Varma. “We have already seen increased allocation towards the rural employment program, higher cooking gas subsidies, and an extension of the food subsidy program.”

After the election, even as the government slows down its capital expenditure, our economists expect private investment to accelerate. Indian companies are well-positioned to do that, Sengupta told CNBC. “Bank balance sheets are well-capitalized, manufacturing balance sheets are deleveraged, and we have a China-plus-one tailwind going on,” he said.

India’s central bank isn’t ready to cut rates in the first half of 2024

This past year, after a deficient monsoon sparked spikes in food inflation, the government took measures to cushion food and oil supply shocks to ensure that they didn’t pinch consumers by feeding into CPI inflation. Exports of rice were suspended, and subsidies on cooking gas and food were extended. Our economists expect food inflation to remain high in the first half of 2024 and expect headline inflation at 5.4% year-over-year during that period, well above the Reserve Bank of India’s target of 4.0%. For the whole year, they expect headline inflation at 4.9%, with core inflation at 4.3%.

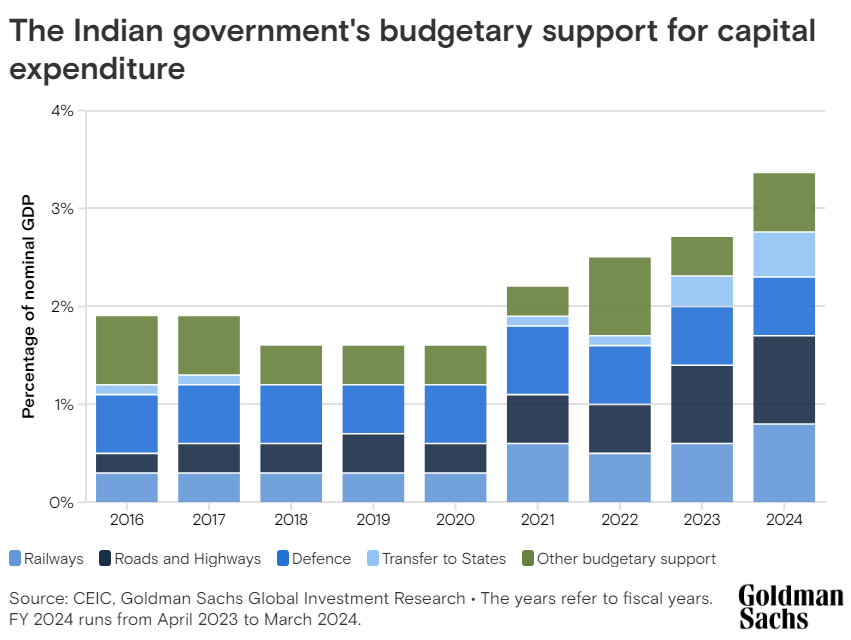

For these reasons, Sengupta told CNBC, the RBI will be slow to cut interest rates. “We have a very shallow rate easing cycle baked into our forecast,” he said. Our economists expect 25 basis points of policy rate cuts each in the third and fourth quarters of 2024. Additionally, they don’t expect the government to widen its fiscal deficit. “The growth in government capex seen in the past few years cannot be sustained going forward, in our view,” write Sengupta and Varma. A decline in public capital expenditure as a share of GDP is likely to accompany other measures aimed at containing the increase in government debt in coming years.

The Indian economy is well-cushioned against external vulnerabilities

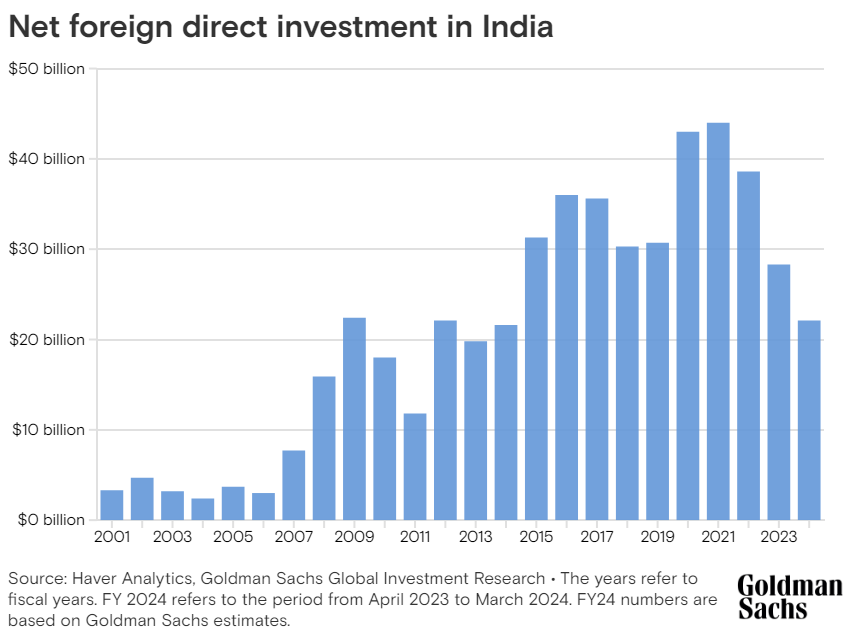

Inflows of foreign direct investment into India are likely to remain muted, in the view of Goldman Sachs economists; net FDI has fallen sharply from a peak of $44 billion in the fiscal year 2020-21, and Goldman Sachs Research estimates that it will drop lower to $22.1 billion in the 2023-24 fiscal year. Slower economic growth among India’s trading partners has impacted its growth of exports in products.

But the export of services has been robust despite weaker demand from western countries, and although growth as a percentage of GDP may have peaked, Sengupta and Varma write, the sector will cushion India’s wide deficit in the trade of goods.

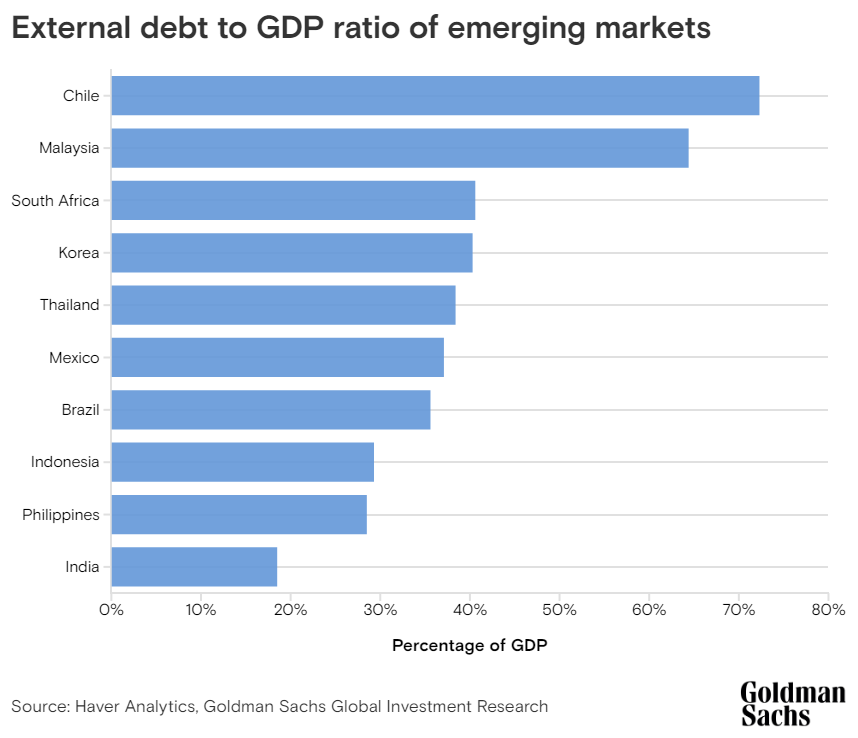

Other aspects of India’s external obligations appear stable or promising as well. India has the lowest external-debt-to-GDP ratio among its peers in the market: around 18%, compared with figures hovering around 40% for South Korea, Thailand, and South Africa. The RBI is also likely to continue intervening in the foreign-exchange market to keep the Indian rupee in a state of low volatility against the dollar.

“Overall, it’s a flattish rupee,” Sengupta told CNBC. The combination of a friendlier Fed, ongoing disinflation, lower oil prices, and still-solid US growth provides a more conducive environment for emerging market assets and currencies. Accordingly, our economists expect the rupee to remain flat over the next three-six months, and expect it to climb to around 81 to the dollar over a 12-month horizon.

This article is being provided for educational purposes only. The information contained in this article does not constitute a recommendation from any Goldman Sachs entity to the recipient, and Goldman Sachs is not providing any financial, economic, legal, investment, accounting, or tax advice through this article or to its recipient. Neither Goldman Sachs nor any of its affiliates makes any representation or warranty, express or implied, as to the accuracy or completeness of the statements or any information contained in this article and any liability therefore (including in respect of direct, indirect, or consequential loss or damage) is expressly disclaimed.